Do you know how often you write out your home address? Maybe you're smart and carry those cute little address stickers which save you time? What you probably don't understand is how your home address is being tracked and even sold by businesses across the US. Like many aspects of our lives, we take our home address for granted while understanding it's importance.

Even though I've moved 14 times since graduating from college, I never understood the problems that occur when you don't have a home address. That is until last year when I decided to leave my husband. I packed my car with critical things I couldn't afford to lose (mostly paperwork). We took a walk where I explained why I was leaving. Having no first hand experience with divorce, I thought I'd be back in a few months to pick up my personal belongings.

This week marks a full calendar year since I left Arizona. The divorce was finalized after 11 months but I'm still living in temporary quarters. That's because I'm building a house and the schedule has slipped three months. So this year has been a roller coaster for many reasons. The home address nightmares though, have added unnecessary stress to my life.

Here are the problems I ran into with my home address … or lack of! For anyone considering a divorce, take these problems very seriously so you can do a better job preparing your new life before you leave home!

Post Office Selling Your New Home Address

One of the first things I did after leaving our Arizona house was to set up mail forwarding. My goal was to get my mail without depending on my estranged husband. So I forwarded my mail to my business post office box. The only problem I found was mail addressed to both of us. The post office told me mail would be sent to the first name on the address.

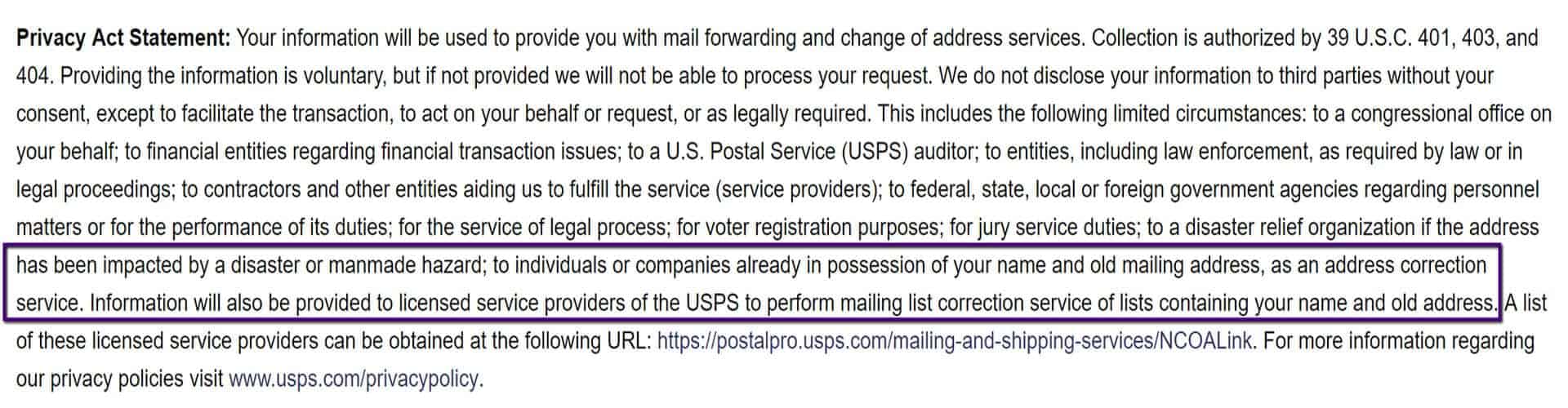

The process seemed easy enough. All you need to do is visit the Official USPS Change of Address website (above). The privacy statement below was easy to read. Unfortunately most people reading the privacy statement (below) was protected but …

I wasn't expecting problems with this simple home address change. Until my cell phone carrier started sending me emails and text messages about a delinquent bill. At first I ignored the messages because the account was on autopay. Finally I logged into the account to check on the credit card and thought everything looked okay.

Next I called to ask why autopay wasn't working. They offered to run the credit card while we were on the phone. Yikes, their system wouldn't accept my credit card. After some discussion we pinpointed the problem. They told me I was giving them the wrong zip code? So I tried different zip codes and discovered the phone company needed the zip code for my new “forward to” address.

Banks Want to Verify Your Home Address

There's good news and bad news here. My original plan was to wait to open new bank accounts until after the divorce was final. That schedule didn't work out because I can't remove my husband from the account. With several of his auto pay withdrawals still hitting my checking account and credit card, I had to pursue new accounts before I was ready.

What I discovered were some great new features that my current credit union doesn't offer. My favorite is your ability to connect to accounts you have with other banks/credit unions, called external accounts. Knowing that I like to move every few years, I decided to pick a bank based on their online services plus 7×24 phone support.

Doing everything online is great. The application process varied quite a bit so I opened several accounts and will stick with those providing the best customer service. And yes, all of them ultimately required me to provide a copy of my drivers license (front and back) to prove my home address.

Mortgage Lenders Want to Confirm Your Home Address (Today & Yesterday)

Financing a home being built is challenging. The builder required me to submit a loan application within a 10 day window after signing the contract (August). My research into interest rates started early January but it's now March and we're still more than 60 days from closing due to multiple schedule slips. So I submitted loan applications to two banks in February. Once drywall is complete I'll be able to pick one of these banks (lowest interest rate, APR and closing costs) and complete my loan.

One of the two banks ran my application through underwriting. Their response asking for lots more documentation prompted this article. This is really happening and I'm thoroughly disgusted at this point. The list (10 items) of new requests. Hope you enjoy reading my response to this item about my home address!

Bank's CREDIT- LETTER OF EXPLANATION FOR:

Alerts have come up stating you could have lived in or owned the following addresses. Please provide a signed letter stating if you lived there, the dates, and if you owned or rented (addresses altered to protect the owners).

- 666 LINDA CT, DAVENPORT, FL

- 2400 OCEAN DR, FT PIERCE, FL

- 5555 EAGLE BLVD, FOUNTAIN HILLS, AZ

Dear Loan Underwriter,

I find this request absurd. Requests should be limited to my finances, both my ability to cover the down payment and closing costs plus monthly mortgage payments. I provided the documents requested by your loan officer. The list was incomplete but after wasting so much time renaming my files to upload into archaic software (20 years old), I decided to stop there.

Where I've lived for the last year has no bearing on my ability to make any mortgage payments. First let me put this in perspective. The house I'm building is house number 15. Over the last forty years I've owned up to five houses at a time. This means I've completed more than 20 closings when you add in refinancing and I've never seen something so ridiculous.

Maybe you've never had a friend who left their marriage and lost their home on doing so? That's what I did in early March, leaving my home in Fountain Hills, Arizona. I've stayed with friends and family over the last year. They live in Arizona, Massachusetts, New Hampshire, Maine, Connecticut, New York, New Jersey, Maryland and Florida. In Florida, I stayed in five different homes.

What's more interesting is who reported these addresses as they only tell you where I received mail, not where I lived!

- My older son when I visited and/or babysat my granddaughter (Davenport, FL). Obviously my credit union reported the mailing address I used to get more checks shipped to my son's house.

- My younger son is the home address (Orlando, FL) provided in my application. I signed the lease when it became clear I needed to put a stake in the ground while my house was being built.

- My college drinking buddy who happened to live in Orlando, as I didn't want to make my divorce a burden for my boys.

- My best friend's snowbird condo (Ft Pierce, FL) as they only stay there for three months each winter. While I didn't pay rent, I did reimburse them for Internet access and higher electric bills. This one is rather interesting as who had this address:

- Fidelity who manages the IBM pension plan.

- Amazon as I ordered books, hangers and possibly a few other things.

- Macy's for two deliveries.

- A family friend who has a spare bedroom. He never asked me to pay rent as he has spent lots of time at my house.

- Arizona house which I've only returned to once since departing early March, to pick up personal belongings.

If you're planning a move or trying to decide if you want to build or buy a home, here are some articles to help you …

Leave a Reply